When AI Makes Fraud Look Real: Takeaways from NMLA

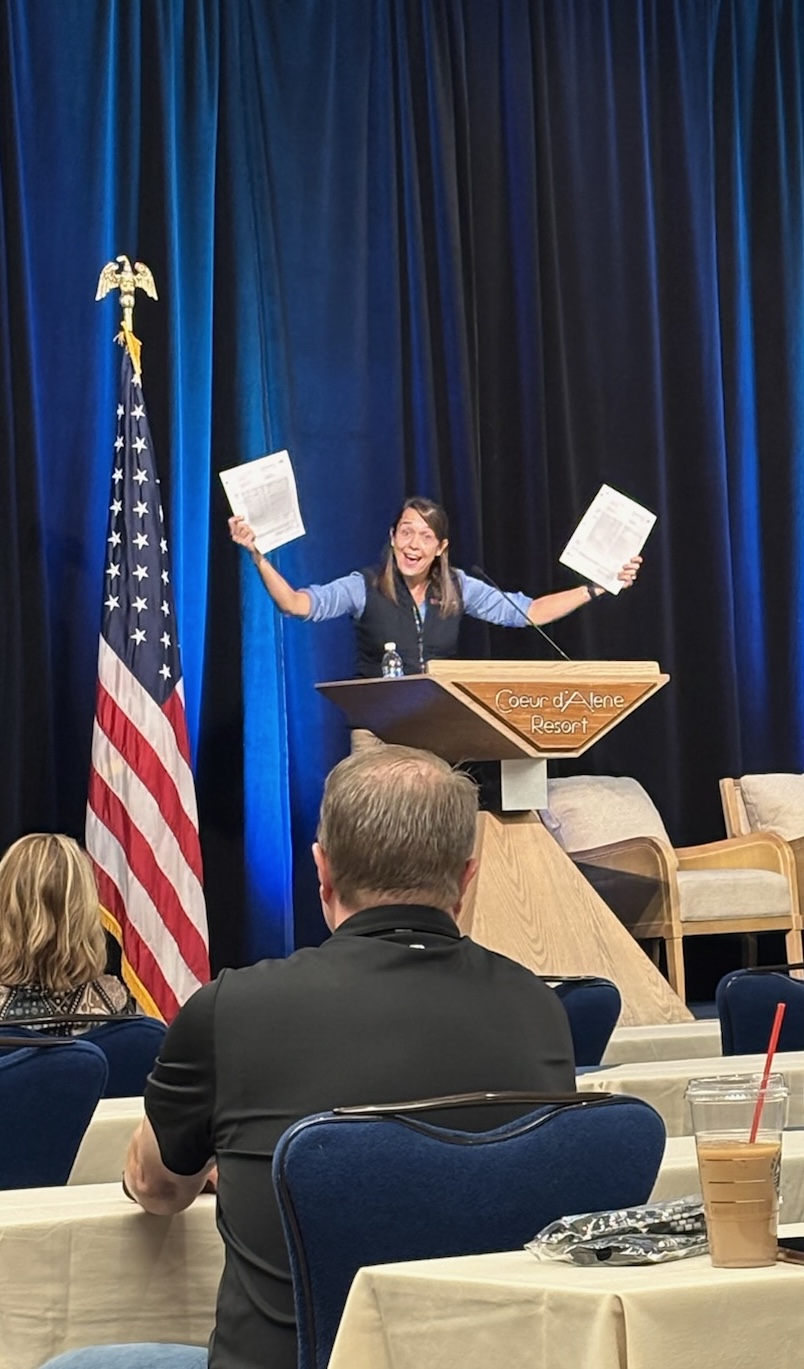

During last month’s National Marine Lenders Association conference in Coeur d’Alene, our Director of Business Development and NMLA Board Member, Caroline Mantel, led a session on fraud in marine lending. To make the risks real, she ran a live experiment. Caroline asked ChatGPT to generate a pay stub that mimics the style of a well known payroll provider. Then she held it up next to an authentic pay stub from that provider. Even in a room full of seasoned lenders, the two were almost indistinguishable at first glance.

That reaction is the story. Document fraud is faster and cheaper with AI, and the “eye test” is no longer enough.

Why this matters to marine lenders

Many fraud schemes start with believable paperwork. Income, employment, insurance, purchase agreements, titles, and even repair invoices can all be fabricated or altered with tools that anyone can use. If your process treats documents as truth rather than as claims to be verified, your risk grows with every application.

The solution is not panic. It is process. Lenders can harden their workflow by pairing document review with independent, trusted data sources and consistent verification steps.

A practical checklist for your team

Use these actions to strengthen your current workflow. You can begin with one or two and build from there.

- Treat documents as claims

Require that every critical fact in a document is verified against an independent source. Examples include employment confirmation from the employer’s official channel, bank verification through approved services, and vessel information validated against authoritative marine data. - Standardize intake

Accept documents only in searchable PDF when possible. Capture metadata on who submitted the file and when it was received. Block images pasted into Word or screenshots that are hard to analyze and archive. - Extract and compare

Pull structured data from pay stubs and other key documents, then compare it across the application. Look for rounding patterns, mismatched dates, inconsistent employer names, or numbers that do not reconcile. Consistency checks catch a large class of basic fakes. - Layer identity and employment verification

Use a consistent playbook for ID proofing and employment checks. Decide in advance which applications trigger secondary review, such as unusually high income relative to role, or employment at firms with limited public footprint. - Verify the vessel, not only the borrower

Cross-check the Hull Identification Number format. Confirm documentation status, title history, and existing liens. Compare listing photos, surveys, and invoices against known events in the vessel’s history. - Keep an audit trail

Log each verification step inside the lending file. A clear trail helps you train staff, identify weaknesses, refine policy, and respond to questions from audit and credit. - Train for AI era red flags

Your staff should know that perfectly aligned typography, uniform spacing, and consistent grayscale do not prove authenticity. Likewise, obvious typos are not required for a document to be fake. The bar has moved.

Where Boat History Report fits

Boat History Report does not verify employment or identity. Our focus is the vessel, which is often where a fraud attempt becomes fragile. We help lenders reduce risk on the asset side by providing:

- HIN validation and pattern checks

- United States Coast Guard documentation status

- Title, registration, and lien insights when available

- Prior damage, insurance, and salvage events

- Ownership history and other data that help match a deal’s story to the vessel’s record

This data gives lenders a second line of defense. Even if a document looks perfect, the vessel’s history can reveal gaps that warrant a closer look.

The Coeur d’Alene experiment, explained

Caroline’s AI pay stub was created for educational purposes using synthetic data. The point was to show how quickly modern tools can produce a convincing artifact that would have looked amateurish just a few years ago. The exercise was not an endorsement of any fraud technique. It was a reminder that our industry must keep pace with the technology that criminals are already using.

What you can do this week

- Pick one loan stage and add a second source of truth. For example, verify HIN and documentation status on every approval folder, not just on higher dollar loans.

- Create a short “in or out” rule for document formats. If a file does not meet your standard, request a resubmission.

- Run a 30 minute refresher with your team on the new red flags that come with AI generated documents.

Closing thought

Fraud has always tried to look ordinary. AI just makes the disguise better. Lenders that combine rigorous document handling with trusted vessel data will be in a stronger position to approve good customers faster and keep bad actors out of their portfolios.